Prepare for Launch

It is officially the start of the Winter Market when buyer demand surges higher, inventory rises at a slower pace, and the market speeds up noticeably.

The Los Angeles housing market is officially transitioning out of the holiday slowdown and into the Winter Market, a period that historically brings a sharp rebound in buyer activity. Each year, demand begins to climb quickly in mid-January as buyers who paused during the holidays return, while new listings increase at a more measured pace. This imbalance between faster-growing demand and slower inventory growth is already beginning to accelerate market activity and shorten decision timelines, even though overall conditions remain more subdued than pre-pandemic norms.

Affordability is playing a meaningful role in this seasonal shift. Mortgage rates have settled notably lower than this time last year, improving purchasing power and encouraging buyers back into the market. While today’s demand levels remain well below historical averages, the trend is clearly upward, with momentum expected to build steadily through late winter and into early spring. Inventory has risen modestly, helped in part by homes re-entering the market after the holidays, but sellers as a group continue to hold back, many waiting for the traditionally stronger spring selling season.

This dynamic has temporarily slowed the market in recent weeks, especially for condos, townhomes, and higher-priced properties, where market times have lengthened more noticeably than for detached homes. The luxury segment, in particular, has cooled as inventory expanded faster than demand, but this phase is typical for January and often followed by gradual improvement as buyer confidence rebuilds. Overall, the message is clear: the Winter Market has arrived, buyer interest is returning, and conditions are setting up for increased activity and competition as Los Angeles heads toward spring.

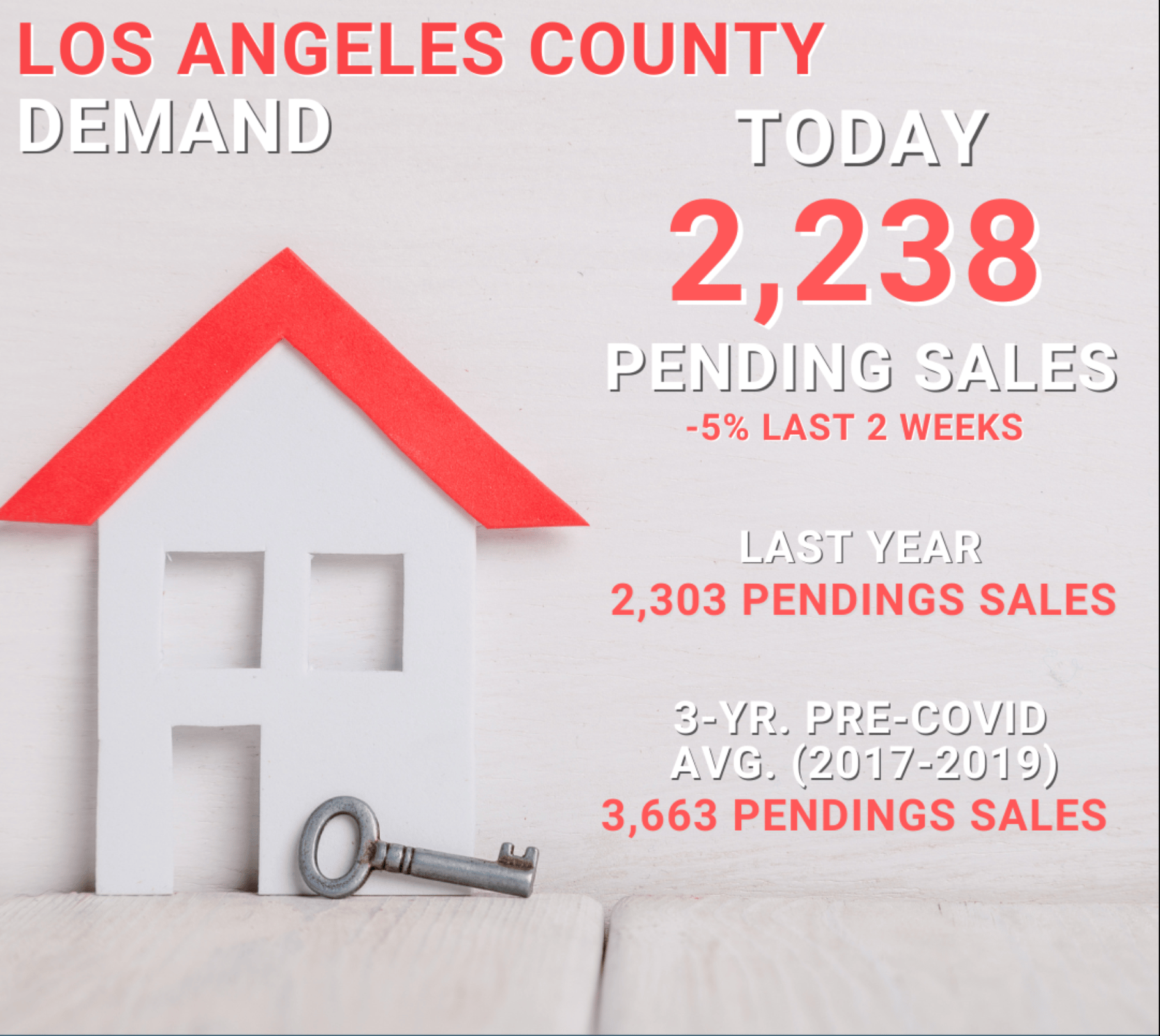

Los Angeles County Housing Summary

- INVENTORY: The active listing inventory over the past couple of weeks increased by 1,333 homes, up 14%, and now stands at 11,041. Last year, there were 9,668 homes on the market, 1,373 fewer homes, or 12% less. The 3-year average before COVID (2017-2019) was 10,633, which is 4% lower. From January through December, 15% fewer homes came on the market compared to the 3-year average before COVID (2017 to 2019), 13,427 less. Yet 6,981 more sellers came on the market this year than last year, and 16,908 more than in 2023.

- DEMAND: Buyer demand, the number of pending sales over the prior month, decreased by 110 in the past two weeks, down 5%, and now totals 2,238. Last year, demand was 2,303 pending sales, 3% more than today. The 3-year average before COVID (2017 to 2019) was 3,663, which is 64% higher.

- MARKET TIME: With supply rising and demand falling, the Expected Market Time, the number of days to sell all Los Angeles County listings at the current buying pace, jumped from 124 to 148 days in the past couple of weeks, its highest mid-January level since tracking began in 2012. Last year, it was 126 days, faster than today. The 3-year average before COVID (2017 to 2019) was 90 days, which is much quicker than today.

- LUXURY: In the past two weeks, the Expected Market Time for homes priced between $2 million and $3 million increased from 153 to 186 days. The Expected Market Time for homes priced between $3 million and $4 million increased from 258 to 371 days. The Expected Market Time for homes priced between $4 million and $8 million increased from 333 to 364 days. The Expected Market Time for homes priced above $8 million increased from 889 to 1,265 days.

- DISTRESSED HOMES: Short sales and foreclosures combined, comprised only 1.4% of all listings and 1.3% of demand. There are 69 foreclosures and 83 short sales available today in Los Angeles County, totaling 152 distressed homes on the active market, up 22 from two weeks ago. Last year, 94 distressed homes were on the market, slightly fewer than today.

- CLOSED SALES: There were 3,848 closed residential resales in December, 1% higher than December 2024’s 3,806 and up 13% from November 2025. The sales-to-list price ratio was 98.4% for Los Angeles County. Foreclosures accounted for 0.7% of all closed sales, and short sales accounted for 0.3%. That means that 99.0% of all sales were sellers with equity.