The Rate Migration

Mortgage rates have crept their way back above 7% with hotter than expected economic readings, resulting in a slowdown in purchase activity.

Rate Sensitivity

The 7% mortgage rate marks a crucial threshold for the housing market's behavior.

TODAY'S RATE: 7.10% (30 Yr. Fixed Rate 2/29/2024)

Prospective buyers closely monitor monthly payments, heavily influenced by prevailing mortgage rates. The housing market witnessed a surge in values as rates plummeted to record lows until 2022. However, as rates soared past 7%, the market became notably sensitive to rate changes, with values showing limited fluctuations despite supply constraints.

Amidst efforts to combat inflation, the Federal Reserve eyes multiple economic indicators, hinting at potential rate cuts. Despite initial expectations for rate drops in 2024, economic reports delay anticipated cuts, causing rates to fluctuate. This uncertainty affects home affordability, with buyers seeing significant shifts in purchasing power based on mortgage rate changes.

Rate sensitivity significantly impacts the housing market, reflecting consumer behavior and broader economic trends.

Active Listings

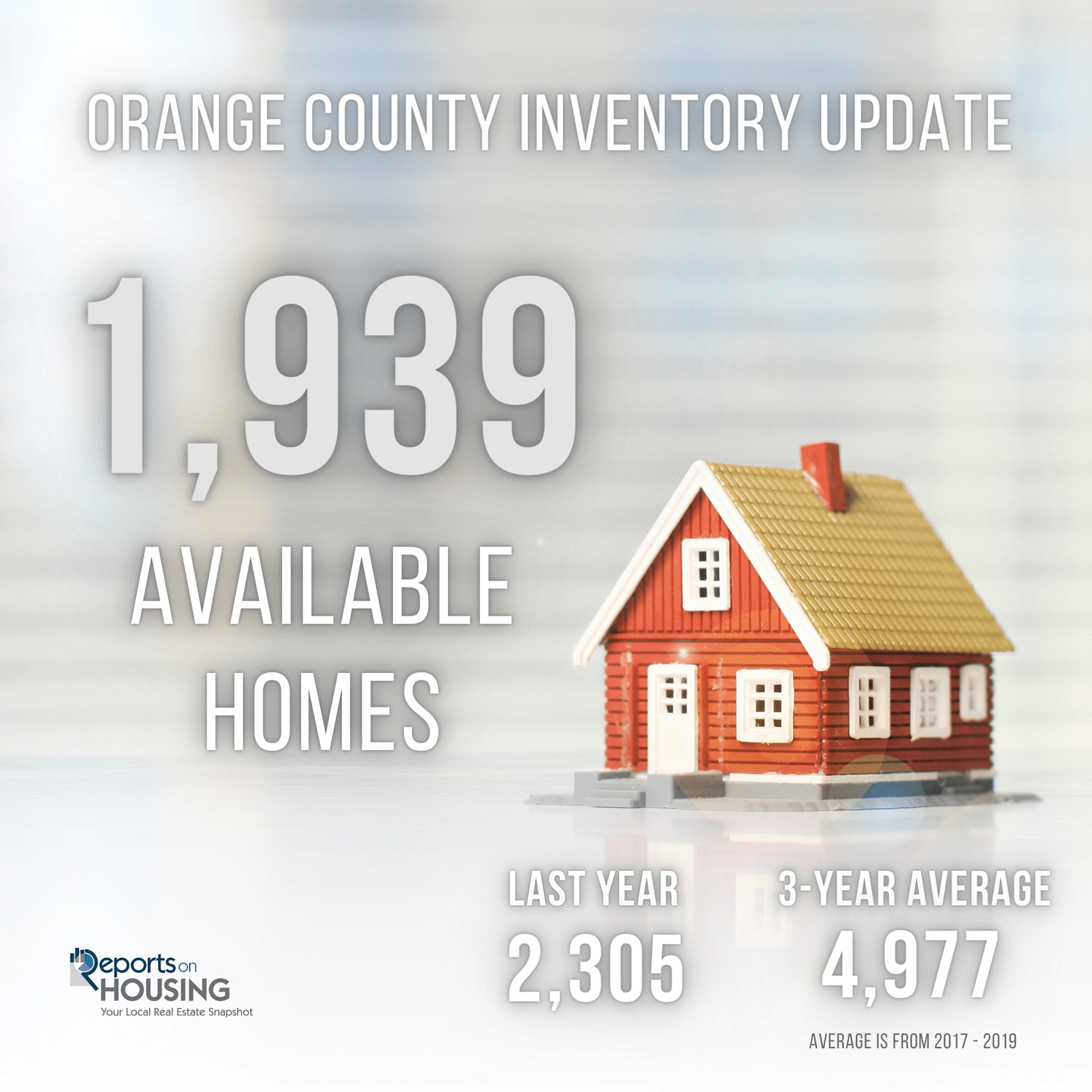

The active listing inventory in the past couple of weeks decreased by three homes, nearly unchanged, and now sits at 1,939. It is the second-lowest mid-February reading since tracking began in 2004, only behind 2022. In January, 35% fewer homes came on the market compared to the 3-year average before COVID (2017 to 2019), 1,072 less. 277 more sellers came on the market this year compared to January 2023. Last year, there were 2,305 homes on the market, 366 more homes, or 19% higher. The 3-year average before COVID (2017 to 2019) was 4,977, or 157% extra, more than double.

Demand

Demand, the number of pending sales over the prior month, increased by 107 pending sales in the past two weeks, up 8%, and now totals 1,397, the lowest mid-February reading since tracking began. Last year, there were 1,537 pending sales, 10% more than today. The 3-year average before COVID (2017 to 2019) was 2,393, or 71% more.

Orange County Housing Summary

- The active listing inventory in the past couple of weeks decreased by three homes, nearly unchanged, and now sits at 1,939. It is the second-lowest mid-February reading since tracking began in 2004, only behind 2022. In January, 35% fewer homes came on the market compared to the 3-year average before COVID (2017 to 2019), 1,072 less. 277 more sellers came on the market this year compared to January 2023. Last year, there were 2,305 homes on the market, 366 more homes, or 19% higher. The 3-year average before COVID (2017 to 2019) was 4,977, or 157% extra, more than double.

- Demand, the number of pending sales over the prior month, increased by 107 pending sales in the past two weeks, up 8%, and now totals 1,397, the lowest mid-February reading since tracking began. Last year, there were 1,537 pending sales, 10% more than today. The 3-year average before COVID (2017 to 2019) was 2,393, or 71% more.

- With demand rising and supply unchanged, the Expected Market Time, the number of days to sell all Orange County listings at the current buying pace, decreased from 45 to 42 days in the past couple of weeks. It was 45 days last year, similar to today. The 3-year average before COVID (2017 to 2019) was 64 days, slower than today.

- For homes priced below $750,000, the Expected Market Time decreased from 36 to 33 days. This range represents 20% of the active inventory and 25% of demand.

- For homes priced between $750,000 and $1 million, the Expected Market Time remained unchanged at 25 days. This range represents 14% of the active inventory and 23% of demand.

- For homes priced between $1 million and $1.25 million, the Expected Market Time decreased from 32 to 31 days. This range represents 9% of the active inventory and 12% of demand.

- For homes priced between $1.25 million and $1.5 million, the Expected Market Time decreased from 39 to 35 days. This range represents 10% of the active inventory and 12% of demand.

- For homes priced between $1.5 million and $2 million, the Expected Market Time decreased from 45 to 44 days. This range represents 12% of the active inventory and 12% of demand.

- For homes priced between $2 million and $4 million, the Expected Market Time in the past two weeks decreased from 80 to 63 days. For homes priced between $4 million and $6 million, the Expected Market Time increased from 133 to 136 days. For homes priced above $6 million, the Expected Market Time decreased from 337 to 240 days.

- The luxury end, all homes above $2 million, account for 35% of the inventory and 16% of demand.

- Distressed homes, both short sales and foreclosures combined, comprised only 0.3% of all listings and 0.3% of demand. Only three foreclosures and two short sales are available today in Orange County, with five total distressed homes on the active market, down two from two weeks ago. Last year, eight distressed homes were on the market, similar to today.

- There were 1,182 closed residential resales in January, up 4% compared to January 2023’s 1,137. December marked a 10% drop compared to December 2023. The sales-to-list price ratio was 98.5% for all of Orange County. Foreclosures accounted for 0.1% of all closed sales, and short sales accounted for 0.1%. That means that 99.8% of all sales were good ol’ fashioned sellers with equity.

Contact me if you are interested in obtaining a comprehensive housing report for Orange County.