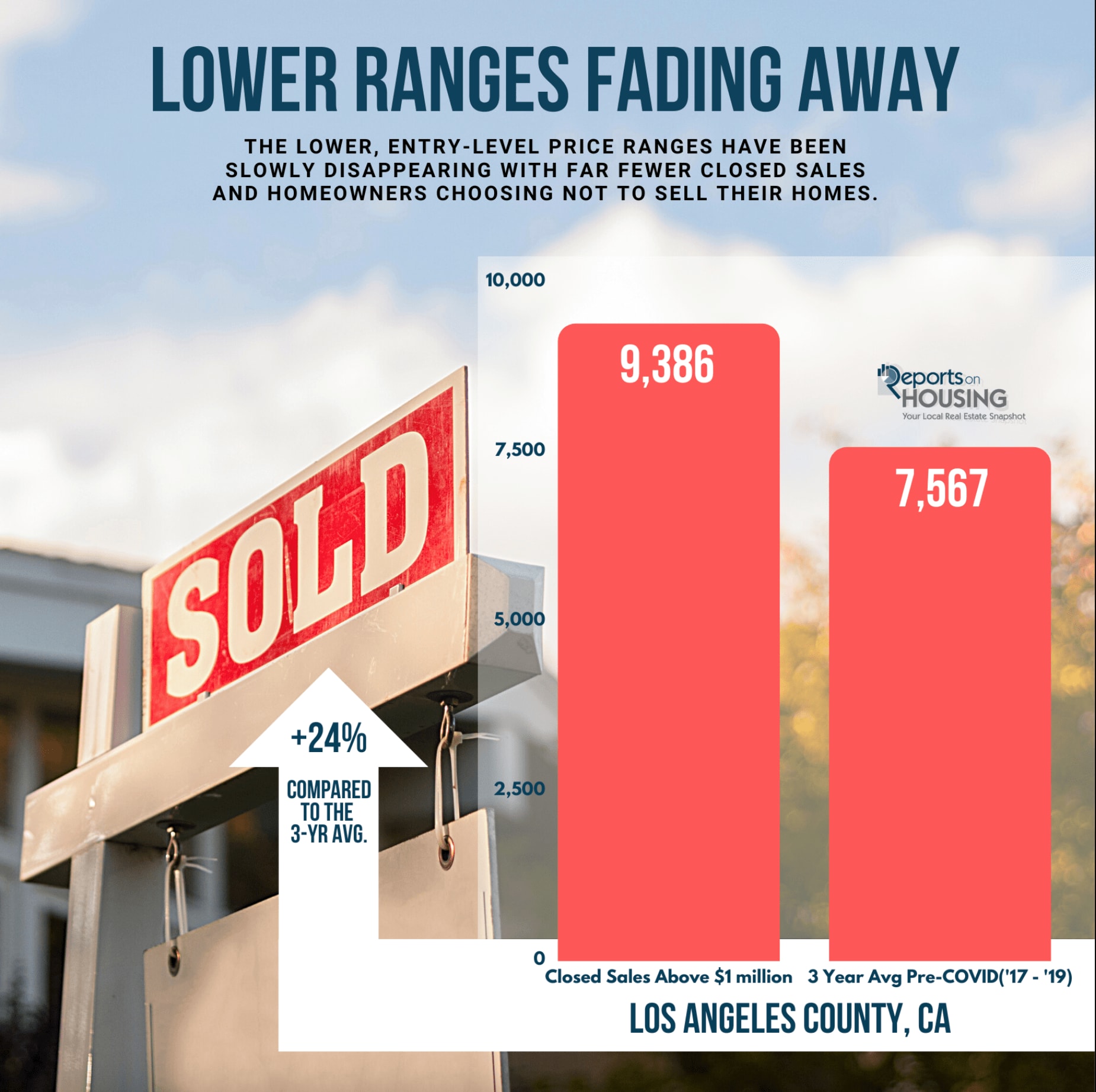

Lower Ranges Fading Away

The lower, entry-level price ranges have been slowly disappearing with far fewer closed sales and homeowners choosing not to sell their homes.

There were an astonishing 44% fewer closed sales and 51% fewer FOR-SALE signs below $1 million this year compared to before COVID.

Thanks to inflation, everyone is paying a lot more for just about everything. From 2019, pre-pandemic, to today, a loaf of bread has increased by 55%. Milk has risen by 31%, ground beef by 34%, and potato chips and a 2-liter soda have soared by 48%. Used cars are up 41%. A Big Mac was priced at $3.79 in 2019 compared to $5.17 today. Wallets have been squeezed. While the inflation rate may be cooling, higher prices are here to stay.

Housing is no exception. According to Freddie Mac’s Home Price Index, since the summer of 2019, the Los Angeles/Orange County metro has increased by 40%. As home prices climbed, what was considered the entry-level to homeownership slowly diminished over time.

Looking at 2013 helps illustrate how the goalposts have been moved for the lower ranges. In 2013, 61% of all closed sales were below $500,000, and 25,752 were detached. In 2019, only 29% were below $500,000, and 9,592 were detached. In 2023 through July, it sank to 3,366, and 1,442 were detached. Buyers today have low expectations in securing a detached home for less than half a million dollars. That price point has faded away.

The data illustrates just how severe the shortage of lower-range homes has become. In 2023, through July, 77% fewer homes were placed on the market below $500,000 compared to the 3-year average before COVID. There were 48% fewer between $500,000 and $750,000. From $750,000 to $1 million, 3% fewer homeowners opted to sell. In total, below $1 million, there have been 21,651 missing FOR-SALE signs. Overall, in Los Angeles County, 36% fewer homes have been placed on the market. Yet above $1 million, there were 6% more sellers, an extra 843. Due to fewer sellers in the lower ranges, the active listing inventory has plunged to unprecedented ultra-low levels, 8,072 homes, the lowest mid-August reading since tracking began in 2012.

Active Inventory

The active listing inventory in the past couple of weeks increased by 233 homes, up 3%, and now sits at 8,072 homes, its highest level since mid-January. It is still the lowest level for mid- August since tracking began in 2012. In July, 35% fewer homes came on the market compared to the 3-year average before COVID (2017 to 2019), 3,025 less. Last year, there were 11,112 homes on the market, 3,040 extra homes, or 38% more. The 3-year average before COVID (2017 to 2019) was 13,288, or 65% more.

Demand

Demand, the number of pending sales over the prior month, decreased by 10 pending sales in the past two weeks, nearly unchanged, and now totals 3,556. Last year, there were 4,278 pending sales, 20% more than today. The 3-year average before COVID (2017 to 2019) was 5,646, or 59% more.

Los Angeles County Housing Summary

- With supply rising and demand unchanged, the Expected Market Time, the number of days to sell all Los Angeles County listings at the current buying pace, increased from 66 to 68 days in the past couple of weeks. It was 78 days last year, slower than today.

- For homes priced below $750,000, the Expected Market Time increased from 42 to 45 days in the past couple of weeks. This range represents 27% of the active inventory and 41% of demand.

- For homes priced between $750,000 and $1 million, the Expected Market Time increased from 48 to 49 days. This range represents 18% of the active inventory and 25% of demand.

- For homes priced between $1 million to $1.5 million, the Expected Market Time increased from 64 to 69 days. This range represents 17% of the active inventory and 17% of demand.

- For homes priced between $1.5 million to $2 million, the Expected Market Time increased from 94 to 99 days. This range represents 10% of the active inventory and 6% of demand.

- For homes priced between $2 million and $3 million, the Expected Market Time in the past couple of weeks decreased from 144 to 128 days. For homes priced between $3 million and $4 million, the Expected Market Time increased from 155 to 162 days. For homes priced between $4 million and $8 million, the Expected Market Time increased from 248 to 281 days. For homes priced above $8 million, the Expected Market Time decreased from 702 to 551 days.

- The luxury end, all homes above $2 million, account for 28% of the inventory and 9.7% of demand.

- Distressed homes, both short sales and foreclosures combined, made up only 0.6% of all listings and 1% of demand. Only 33 foreclosures and 17 short sales are available to purchase today in all of Los Angeles County, 50 total distressed homes on the active market, up one in the past two weeks. Last year there were 39 total distressed homes on the market, slightly fewer than today.

- There were 3,804 closed residential resales in July, 17% less than July 2022’s 4,604 closed sales. July marked a 17% drop compared to June 2023. The sales-to-list price ratio was 100.7% for all of Los Angeles County. Foreclosures accounted for just 0.5% of all closed sales, and short sales accounted for 0.2%. That means that 99.3% of all sales were good ol’ fashioned sellers with equity.