Sluggish Intro to 2023

In contrast to the extraordinary and unprecedentedly high levels of activity seen at the beginning of 2021 and 2022, the start of this year has been characterized by low demand, limited inventory, and market conditions similar to those prior to the pandemic.

2023 Start

With very little demand and a subdued inventory, real estate activity will be suppressed as the year gets underway. Homeowners continue to “hunker down” in their homes, not willing to move due to their current underlying, locked-in, low fixed-rated mortgage. The difference between their low fixed rate and today’s rate is quite large and precludes many homeowners from listing their homes for sale and moving to another home. This will continue until mortgage rates drop.

Los Angeles County Annual Housing Start

With heightened demand and a low supply of available homes, the Expected Market Time, the time between pounding in the FOR-SALE sign to opening escrow, dropped to record low levels, 53 days in 2021 and 38 days in 2022. Today, the inventory might be at the third lowest level to start a year behind the pandemic years of 2021 and 2021, but when it is combined with record low demand, the Expected Market Time is no longer at insane levels.

Demand and Supply

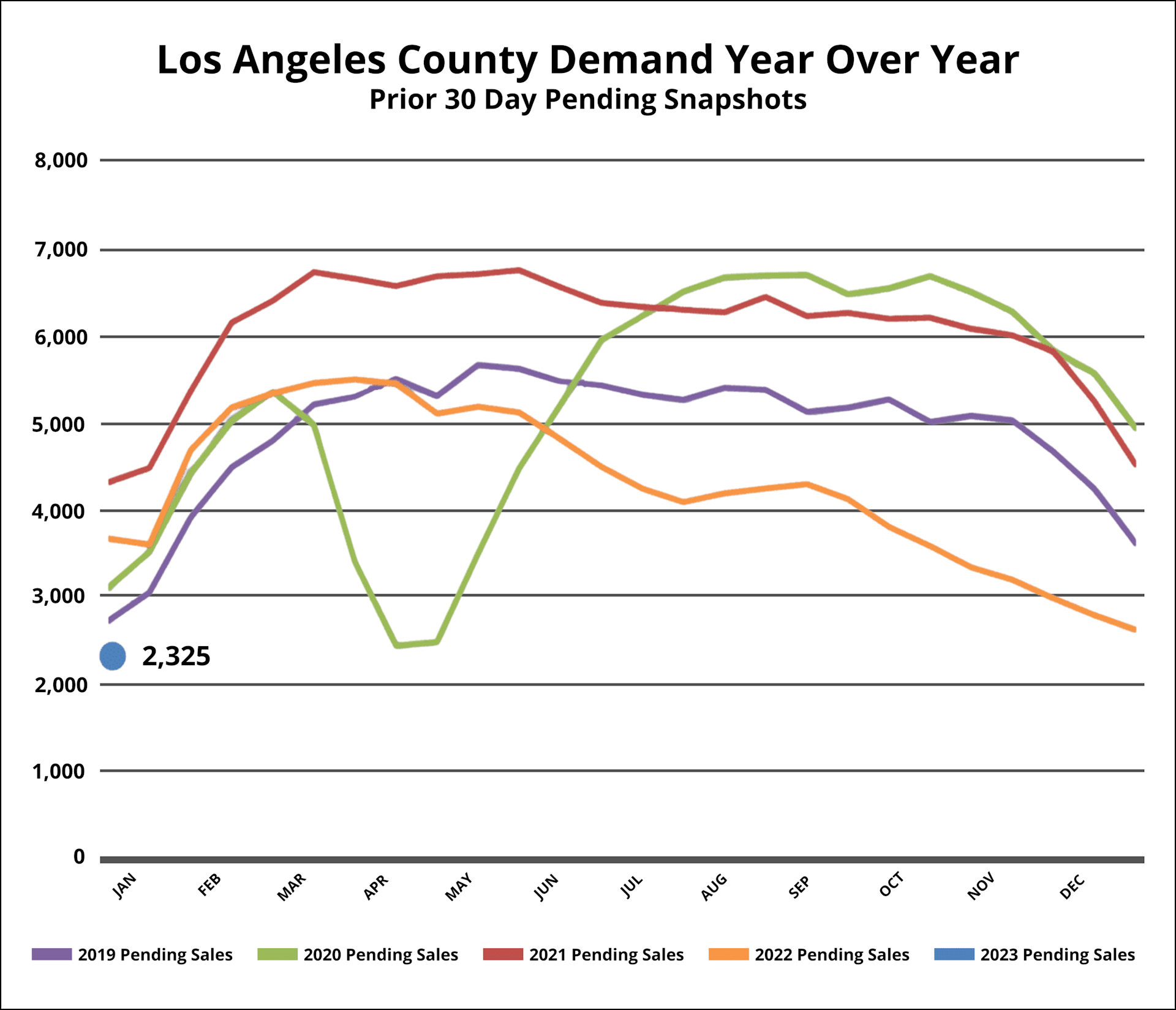

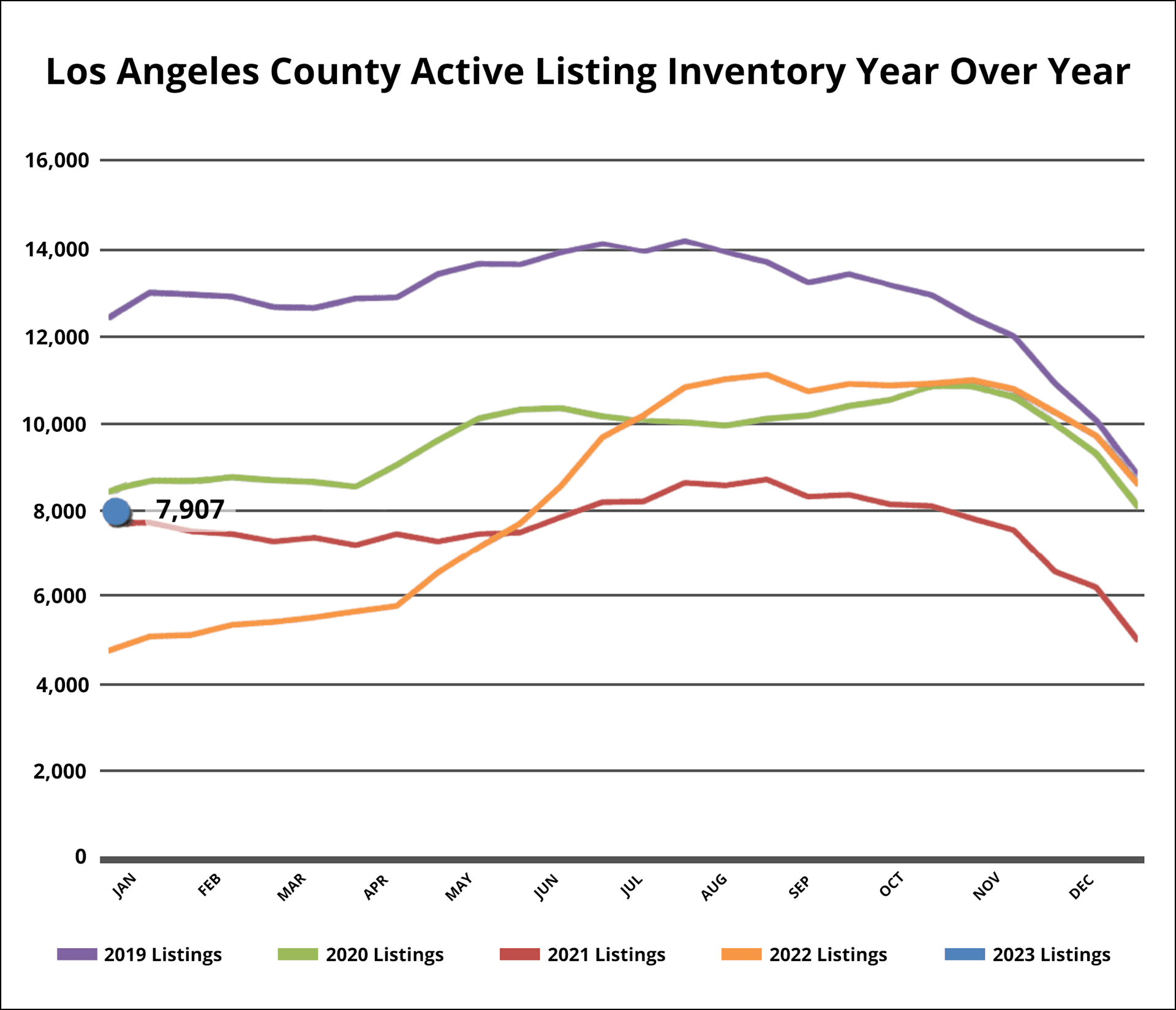

Demand, a snapshot of the number of new escrows over the prior month, plunged from 2,661 to 2,325 in the past couple of weeks, shedding 336 pending sales, or down 13%. Last year, demand was at 3,703, 59% more than today, or an extra 1,378. The 3-year average prior to COVID (2017 to 2019) was at 3,033 pending sales, 30% more than today. The active listing inventory decreased by 705 homes in the past couple of weeks, down 8%, and now sits at 7,907 homes. On January 1st there were 7,664 homes, the third lowest level to start the year since tracking began 11 years ago. Only the pandemic years of 2021 and 2022 were lower. Since New Year’s Day, the inventory has risen by 3%, adding 243 homes. Last year, the inventory was at 4,732, 40% lower, or 3,175 fewer. The 3-year average prior to COVID (2017 to 2019) is 9,751, an extra 1,844 homes, or 23% more. There were more choices back then.