Scraping the Bottom

The active inventory, buyer demand, and the number of homeowners willing to sell have been bouncing around a bottom all year, so it is only up from here.

Low Readings for a Year Now

Housing is finally at a point where year-over-year statistics will isolate the slightest signs of improvement in the housing market.

Peanut butter, a delightful treat on crackers, toast, or cookies, often leaves us scraping the jar for every last bit. Similarly, the housing market resembles that nearly empty jar, with extremely low supply, and buyer demand, all affected by soaring mortgage rates post-COVID. Despite this year-long stagnation, any upward movement in these factors will shape the market's direction significantly.

The housing scenario in 2023 witnessed record-high mortgage rates reaching above 7%, plunging demand and inventory levels. Homeowners, dissuaded by the high rates, showed reluctance to sell, with new sellers dropping by significant percentages compared to pre-COVID averages. This year's market has remained subdued, barely fluctuating, as mortgage rates deter potential sellers and flatten the available inventory.

Looking ahead, the market anticipates a shift. As the economy is expected to cool in 2024, investors might seek safer investments, leading to a potential decline in mortgage rates. A drop in rates could spark increased buyer demand and prompt more homeowners to sell, ultimately altering the housing market's landscape. This stagnant phase won't persist indefinitely; changes are imminent, resembling the opening of a new jar of peanut butter.

Active Listing

The active listing inventory in the past couple of weeks plunged by 187 homes, down 7%, and now sits at 2,309, its lowest level since the start of July. It was also the largest drop of the year. In October, 36% fewer homes came on the market compared to the 3-year average before COVID (2017 to 2019), 1,093 less. Last year, there were 3,286 homes on the market, 977 more homes, or 42% higher. The 3-year average before COVID (2017 to 2019) was 5,359, or 132% extra, more than double.

Demand

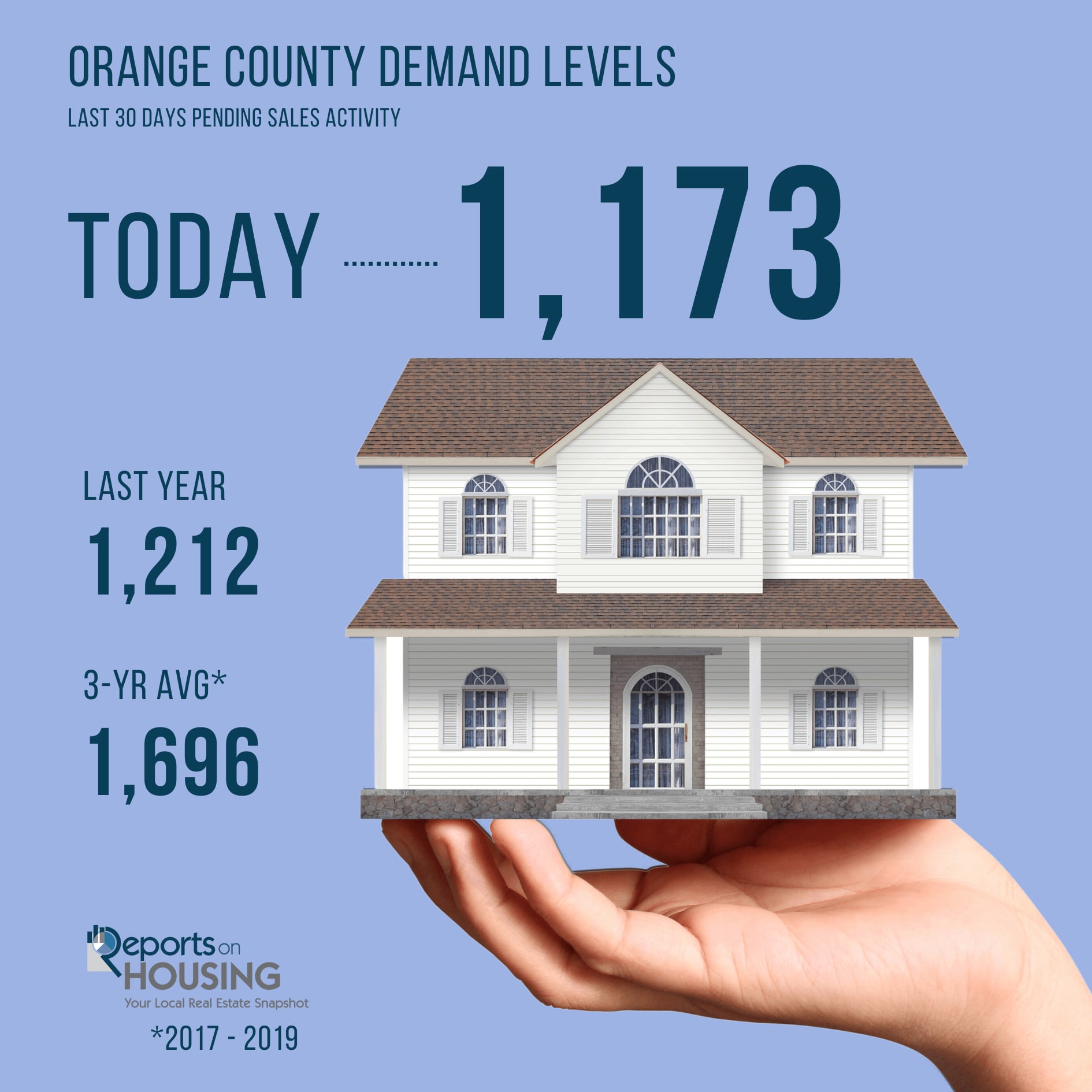

Demand, the number of pending sales over the prior month, decreased by 50 pending sales in the past two weeks, down 4%, and now totals 1,173, its lowest level since tracking began in 2004. Last year, there were 1,212 pending sales, 3% more than today. The 3-year average before COVID (2017 to 2019) was 1,969, or 68% more.

Orange County Housing Summary

- With the inventory plunging faster than demand, the Expected Market Time, the number of days to sell all Orange County listings at the current buying pace, decreased from 61 to 59 days in the past couple of weeks. It was 81 days last year, slower than today. The 3-year average before COVID (2017 to 2019) was 85 days, also slower than today.

- For homes priced below $750,000, the Expected Market Time decreased from 45 to 41 days. This range represents 19% of the active inventory and 27% of demand.

- For homes priced between $750,000 and $1 million, the Expected Market Time decreased from 41 to 38 days. This range represents 16% of the active inventory and 24% of demand.

- For homes priced between $1 million and $1.25 million, the Expected Market Time decreased from 46 to 44 days. This range represents 10% of the active inventory and 14% of demand.

- For homes priced between $1.25 million and $1.5 million, the Expected Market Time decreased from 46 to 44 days. This range represents 9% of the active inventory and 12% of demand.

- For homes priced between $1.5 million and $2 million, the Expected Market Time decreased from 70 to 68 days. This range represents 13% of the active inventory and 11% of demand.

- For homes priced between $2 million and $4 million, the Expected Market Time in the past two weeks increased from 103 to 115 days. For homes priced between $4 million and $6 million, the Expected Market Time increased from 231 to 240 days. For homes priced above $6 million, the Expected Market Time decreased from 469 to 444 days.

- The luxury end, all homes above $2 million, account for 33% of the inventory and 12% of demand.

- Distressed homes, both short sales and foreclosures combined, comprised only 0.3% of all listings and 0.1% of demand. Only six foreclosures and two short sales are available today in Orange County, with eight total distressed homes on the active market, up two from two weeks ago. Last year, eight distressed homes were on the market, identical to today.

- There were 1,632 closed residential resales in October, 5% less than October 2022’s 1,726 closed sales. October marked a 1% drop compared to September 2023. The sales-to-list price ratio was 98.9% for all of Orange County. Foreclosures accounted for 0.1% of all closed sales, and there were no closed short sales. That means that 99.9% of all sales were good ol’ fashioned sellers with equity.

Contact me for the complete Orange County Housing Report.